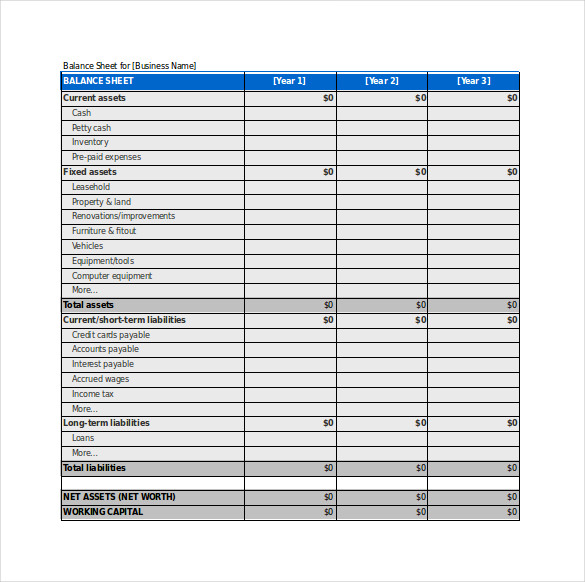

Hey weird 4ns, you and Iz combined don't have half of the equity, or cash, on my balance sheet. Wanna bet? No, you don't. I don't blame you.

First you have to have Money " Messy ".....

Hey weird 4ns, you and Iz combined don't have half of the equity, or cash, on my balance sheet. Wanna bet? No, you don't. I don't blame you.

Somebody's jeaaalllous!

Believe me, I understand.

And that's why you won't bet me! Coward.

Thanks for letting me know.Only a Fool does what you're doing on this forum.

The hallmark of a truly free market is that all associations and relationships are based on voluntary agreement and mutual consent. Another way of saying this is that, in the free market society, people are morally and legally viewed as sovereign individuals possessing rights to their life, liberty, and honestly acquired property, who may not be coerced into any transaction that they do not consider to be to their personal betterment and advantage.

The rules of the free market are really very simple: you don’t kill, you don’t steal, and you don’t cheat through fraud or misrepresentation. You can only improve your own position by improving the circumstances of others. Your talents, abilities, and efforts must all be focused on one thing: what will others take in trade from you for the revenues you want to earn as the source of your own income and profits?

Consent, Not Coercion, Is a Hallmark of the Market

https://fee.org/articles/free-markets-refine-good-manners/

What is the hallmark of a monopoly or a cartel?

Who said I support the higher taxes that tariffs are, which is the Democrats battle cry for 2020? You people are easily confused and detest the details of the difference between QE and Tariffs. Funny how you people support one while detesting the other. Though they both generate future cost, one is in the billions while the other is senselessly in the trillions. ....your hater is on overload.What is the hallmark of a monopoly or a cartel?

Thank you Mr. Econ 99. How is your hero Trump doing with all of this? Trump is a fucking moron when it comes to Free Trade and you are here every day defending the jackass. You are one confused tool.

From the article:

"The difference between the lower price the consumer would pay under free trade, and the higher price they would pay under a tariff, is the stolen sum out of the consumer's pocket."

Trump knows this but he keeps lying about it to his base of idiots becuase he knows how ignorant his they are. Case in point - the nutters on this board.

Please carry on with your confusion Izzy - its very entertaining.

QE is a tax on the country’s citizens, creating fiat money to raise revenue for operating the government.Tariffs are a tax on a country's citizens to raise revenue for operating the government (including the part of the government that decides how much tariff to apply) or to influence their buying decisions. Tariffs only affect other countries when the tariffs are high enough to discourage imports, or perhaps when tariffs are applied selectively to one country's exports compared to those from another.

In the early days of our Republic, the chief sources of income for the government were land sales and tariffs.

QE is a tax on the country’s citizens, creating fiat money to raise revenue for operating the government.

Your powers of non-deduction in action.Nonsense.

Wrong! You have to be able to do third grade math first. Said he had to go to his weekend home to get his CLTV. That was one of his best yet.First you have to have Money " Messy ".....

Thanks for letting me know.

Speaking of fools, tell me about the child molesting DC Democrat pizza parlor again? That was you who talked about it as fact, right?

Deflection, of course.QE is a tax on the country’s citizens, creating fiat money to raise revenue for operating the government.

It's better then hiding in a corner like you...Deflection, of course.

Actually, rare agreement with your father although I’m sure your father did not intend to agree on taxes Imposed on citizens. No wonder Fries U rejected your application.Deflection, of course.